Planning for retirement can feel daunting, a vast landscape of investment options and financial strategies. This guide navigates you through the essential steps, from defining your retirement goals and assessing your risk tolerance to selecting appropriate investment vehicles and developing a robust withdrawal plan. We’ll explore diverse strategies to help you build a secure financial future, ensuring you enjoy the retirement you envision.

Understanding your personal financial situation is the cornerstone of successful retirement planning. We’ll delve into the intricacies of various investment vehicles, emphasizing the importance of diversification and risk management. This guide empowers you to make informed decisions, whether you’re a seasoned investor or just starting your retirement savings journey.

Assessing Risk Tolerance

Understanding your risk tolerance is crucial for making sound investment decisions. It’s about determining the level of potential loss you’re comfortable accepting in pursuit of higher returns. This assessment involves considering several key factors, and a careful evaluation will help you choose investments that align with your financial goals and personal comfort level. Ignoring your risk tolerance can lead to significant financial stress and potentially derail your retirement plans.

A practical method for determining your risk tolerance involves a self-assessment considering your age, income, financial goals, and time horizon. Younger investors with longer time horizons often have a higher risk tolerance, as they have more time to recover from potential market downturns. Conversely, those nearing retirement typically prefer lower-risk investments to preserve their capital. Your income also plays a role; higher earners might be more comfortable with riskier investments, while those with lower incomes may prioritize capital preservation.

Finally, your investment goals – whether it’s aggressive growth or steady income – significantly influence your risk tolerance.

Risk Tolerance Assessment Process

A flowchart can visually represent the process of assessing risk tolerance and selecting appropriate investments. Imagine a flowchart beginning with a question: “What is your age and time horizon until retirement?”. This branches into three paths: “Short-term (less than 5 years)”, “Medium-term (5-10 years)”, and “Long-term (more than 10 years)”. Each path leads to a subsequent question regarding income stability and financial goals.

For example, a “short-term” path might lead to a question about the level of capital preservation needed, while a “long-term” path might focus on growth potential. Each answer further refines the risk profile, ultimately leading to recommended investment options. For example, a long-term investor with high income and aggressive growth goals might be directed towards a portfolio heavily weighted in stocks, while a short-term investor prioritizing capital preservation might be advised to invest primarily in bonds and money market accounts.

Consequences of Mismatched Risk Profiles

Investing outside your risk tolerance can have serious repercussions. For instance, a risk-averse investor heavily invested in volatile stocks during a market downturn could experience significant anxiety and potential financial losses, undermining their retirement security. Conversely, a risk-tolerant investor who invests conservatively might miss out on substantial potential gains over the long term. The key is to find a balance between risk and reward that aligns with your individual circumstances and comfort level.

Consider a hypothetical scenario: an individual nearing retirement invests heavily in high-growth tech stocks. A market correction could severely impact their retirement savings, potentially leaving them with insufficient funds. Alternatively, a younger investor with a high risk tolerance investing solely in low-yield bonds might find their retirement savings growing too slowly to meet their long-term goals.

Investment Vehicles for Retirement

Choosing the right investment vehicle is crucial for securing your financial future in retirement. Different options cater to varying risk tolerances, income needs, and tax situations. Understanding the nuances of each vehicle will help you make informed decisions aligned with your personal financial goals.

Comparison of Retirement Investment Vehicles

The primary retirement investment vehicles available are 401(k)s, Traditional IRAs, and Roth IRAs. Each offers unique benefits and drawbacks. Careful consideration of these factors is essential before selecting the best fit for your circumstances.

- 401(k)s: Employer-sponsored retirement savings plans that often include employer matching contributions. Contributions are typically made pre-tax, reducing your taxable income in the present.

- Traditional IRAs: Individual Retirement Accounts where contributions are made pre-tax, reducing your taxable income in the present. There are annual contribution limits.

- Roth IRAs: Individual Retirement Accounts where contributions are made after-tax, meaning you pay taxes now but withdrawals in retirement are tax-free.

Tax Implications of Retirement Investment Vehicles

Tax implications significantly influence the long-term value of your retirement savings. Understanding these differences is vital for maximizing your after-tax returns.

- 401(k)s: Contributions are tax-deductible, reducing your current taxable income. However, withdrawals in retirement are taxed as ordinary income.

- Traditional IRAs: Similar to 401(k)s, contributions are tax-deductible, lowering your current tax liability. Withdrawals in retirement are taxed as ordinary income.

- Roth IRAs: Contributions are not tax-deductible, meaning you pay taxes upfront. However, qualified withdrawals in retirement are tax-free, providing a significant advantage in the long run. This includes both the contributions and the earnings.

Advantages and Disadvantages of Retirement Investment Vehicles

Each retirement vehicle presents a unique set of advantages and disadvantages. Consider your financial situation, risk tolerance, and long-term goals when evaluating these factors.

- 401(k)s:

- Advantages: Employer matching contributions, potential for tax advantages, convenience of automatic payroll deductions.

- Disadvantages: Limited investment choices compared to IRAs, potential for high fees depending on the plan provider, vesting requirements (employer contributions may not be fully yours until you’ve worked a certain number of years).

- Traditional IRAs:

- Advantages: Wide range of investment options, tax-deductible contributions, potential for tax-deferred growth.

- Disadvantages: Taxed upon withdrawal, income limitations may restrict eligibility for tax deductions, early withdrawal penalties may apply.

- Roth IRAs:

- Advantages: Tax-free withdrawals in retirement, no required minimum distributions (RMDs), potential for higher after-tax returns over time.

- Disadvantages: No tax deduction for contributions, income limitations may restrict eligibility, potential for lower returns in the early years due to paying taxes upfront.

Diversification Strategies

Diversification is a cornerstone of sound retirement planning. It’s the practice of spreading your investments across various asset classes to reduce the overall risk of your portfolio. By not putting all your eggs in one basket, you lessen the impact of any single investment performing poorly. This strategy aims to maximize returns while minimizing potential losses.Diversification helps to manage volatility and potentially enhance long-term growth.

A well-diversified portfolio is less susceptible to market fluctuations in any single sector or asset class. This is particularly crucial during retirement, when you’re relying on your investments for income.

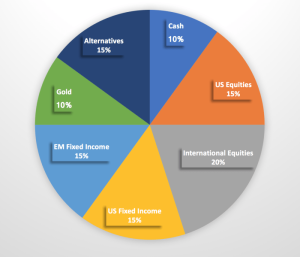

Portfolio Diversification Examples

The following table illustrates examples of diversified portfolios across different asset classes. Remember that these are examples and the optimal allocation will depend on individual circumstances, including age, risk tolerance, and financial goals.

| Portfolio Name | Stocks (%) | Bonds (%) | Real Estate (%) | Other (%) |

|---|---|---|---|---|

| Conservative Portfolio | 20 | 60 | 10 | 10 (e.g., Cash, Annuities) |

| Balanced Portfolio | 40 | 40 | 10 | 10 (e.g., Commodities, Alternative Investments) |

| Growth Portfolio | 70 | 20 | 5 | 5 (e.g., Emerging Markets, Private Equity) |

| Aggressive Growth Portfolio | 80 | 10 | 5 | 5 (e.g., High-Yield Bonds, Venture Capital) |

Asset Allocation Adjustment Based on Age and Risk Tolerance

Asset allocation should be adjusted over time to reflect changes in age and risk tolerance. Generally, younger investors with a longer time horizon can tolerate more risk and therefore allocate a larger portion of their portfolio to stocks. As investors approach retirement, they typically shift towards a more conservative allocation with a greater emphasis on bonds and less volatile investments to preserve capital.For example, a 30-year-old investor might comfortably hold a growth portfolio with a higher percentage allocated to stocks, while a 60-year-old investor nearing retirement might prefer a balanced or conservative portfolio with a larger proportion in bonds to reduce risk.

A more risk-averse investor, regardless of age, might always prefer a more conservative portfolio with lower stock exposure. Conversely, a risk-tolerant investor might maintain a higher stock allocation even closer to retirement. The key is to align the portfolio with one’s comfort level and financial goals.

Investment Advice

Planning for a comfortable retirement involves navigating the complex world of investments. While self-directed investing is possible, seeking professional financial advice is often crucial for optimizing your retirement portfolio and mitigating potential risks. A well-structured plan considers your individual circumstances, goals, and risk tolerance to create a strategy that maximizes your chances of achieving your retirement objectives.Understanding the importance of professional financial advice is paramount.

A qualified financial advisor brings expertise, objectivity, and a comprehensive understanding of market dynamics that the average investor may lack. They can help you navigate the intricacies of investment choices, diversification strategies, and risk management, ultimately leading to better-informed decisions.

Factors Considered in Retirement Investment Planning

A comprehensive retirement investment plan requires careful consideration of several key factors. Your financial advisor should assess your current financial situation, including assets, debts, and income. They will also delve into your long-term goals, such as desired retirement lifestyle and expected expenses. Crucially, your risk tolerance—your comfort level with potential investment losses—will heavily influence the asset allocation within your portfolio.

Time horizon, the period until retirement, is another significant factor; longer time horizons generally allow for greater risk-taking. Finally, tax implications of various investment choices must be carefully considered to maximize after-tax returns.

Red Flags in Investment Advice

It is essential to be vigilant about potential red flags when considering investment advice. Unsubstantiated high returns, unrealistic promises, or pressure to invest quickly should raise serious concerns. Similarly, lack of transparency about fees or investment strategies, or claims of guaranteed returns, are warning signs of potential scams or unsuitable investments. Always verify credentials and experience, and be wary of advisors who push specific products without considering your individual needs.

- Guarantees of high returns: No investment guarantees high returns without significant risk.

- High-pressure sales tactics: Legitimate advisors prioritize client needs over immediate sales.

- Lack of transparency regarding fees: All fees and commissions should be clearly disclosed.

- Unregistered or unlicensed advisors: Verify credentials with relevant regulatory bodies.

- Unsolicited investment advice: Be cautious of unsolicited calls or emails promoting investments.

Managing Retirement Investments

Successfully navigating retirement requires a proactive approach to managing your investments. Your investment strategy shouldn’t be static; it should evolve alongside your changing circumstances and the ever-shifting market landscape. A well-defined plan, incorporating regular adjustments, is crucial to ensuring you meet your financial goals throughout retirement.

Effective management hinges on understanding your risk tolerance at different life stages and adapting your portfolio accordingly. As you approach and enter retirement, your priorities and time horizon change, influencing your investment choices and risk appetite. Regular monitoring and rebalancing are essential components of this dynamic process.

Investment Strategies Across Life Stages

Retirement investment management isn’t a one-size-fits-all approach. Your strategy should adapt as you move through different phases of retirement. For instance, in the early years of retirement, you might have a longer time horizon and a higher tolerance for risk, allowing for a more aggressive investment strategy focused on growth. However, as you age and your need for income increases, a more conservative approach with a focus on preservation of capital becomes more prudent.

Consider a hypothetical example: A 65-year-old retiree with a large nest egg and a long life expectancy might allocate a significant portion of their portfolio to equities for growth, while a 85-year-old retiree with a shorter time horizon and greater need for income might prefer a higher allocation to fixed-income investments such as bonds and certificates of deposit.

The Importance of Portfolio Rebalancing

Regular portfolio rebalancing is a crucial aspect of managing retirement investments. Rebalancing involves adjusting your asset allocation back to your target percentages after market fluctuations. Over time, some asset classes will outperform others, leading to deviations from your original plan. Rebalancing helps you to maintain your desired level of risk and avoid becoming overly concentrated in any single asset class.

For example, if your target allocation is 60% stocks and 40% bonds, and the market experiences a period of strong stock performance, your portfolio might become 70% stocks and 30% bonds. Rebalancing would involve selling some stocks and buying bonds to restore the 60/40 ratio. This disciplined approach helps to reduce risk and capitalize on market inefficiencies.

Adjusting Investment Strategies to Market Fluctuations

Market fluctuations are inevitable. A well-defined plan should include strategies for navigating both bull and bear markets. During periods of market volatility, it’s essential to avoid impulsive decisions driven by fear or greed. Instead, focus on your long-term goals and consider the following strategies:

During a market downturn, consider increasing your contributions to take advantage of lower prices. Conversely, during a market upswing, you may want to consider rebalancing your portfolio to reduce exposure to riskier assets. Remember, market timing is notoriously difficult, so a long-term perspective and a well-diversified portfolio are your best defenses against market fluctuations.

Withdrawal Strategies in Retirement

Planning for withdrawals from your retirement accounts is crucial for ensuring a comfortable and financially secure retirement. A well-designed withdrawal strategy considers several key factors, including your expected lifespan, the rate of inflation, your desired lifestyle, and your overall financial health. Failing to account for these factors could lead to running out of funds prematurely or needing to drastically reduce your spending in later years.

A successful withdrawal strategy is not a one-size-fits-all solution; it’s a personalized plan tailored to your specific circumstances. It involves carefully balancing your need for income with the need to preserve your capital to protect against unexpected expenses or prolonged lifespans. The goal is to create a sustainable income stream that allows you to maintain your desired standard of living throughout retirement.

Factors Influencing Withdrawal Strategies

Several factors significantly impact the design of a retirement withdrawal strategy. These include longevity (how long you’ll live in retirement), inflation (the erosion of purchasing power over time), tax implications (how withdrawals are taxed), and your risk tolerance (your comfort level with potential investment losses). A comprehensive plan considers all these aspects to minimize risk and maximize the longevity of your retirement funds.

For example, someone expecting a longer retirement may opt for a more conservative withdrawal strategy than someone with a shorter projected retirement timeframe. Similarly, someone with a higher risk tolerance might consider a more aggressive approach, while someone with a lower risk tolerance would prefer a more conservative one.

Comparison of Different Withdrawal Strategies

Different withdrawal strategies aim to balance income needs with capital preservation. The choice depends on individual circumstances and risk tolerance.

- Fixed-Income Strategy: This involves withdrawing a fixed amount each year, regardless of market performance. This provides predictable income but may not keep pace with inflation if returns are low. For example, a retiree might withdraw $50,000 annually. This strategy offers simplicity and predictability but carries the risk of depleting funds early if investment returns are poor or the retiree lives longer than expected.

- Variable-Income Strategy: This involves adjusting withdrawals based on investment performance. In good years, withdrawals might be higher; in poor years, they might be lower. This approach aims to protect principal but requires greater flexibility and careful monitoring. A variable income strategy might involve withdrawing 4% of the portfolio’s value annually, adjusting the amount each year based on the portfolio’s performance.

This offers a degree of inflation protection but requires more active management and can be more complex.

- Systematic Withdrawal Plan (SWP): This strategy involves systematically withdrawing a predetermined percentage of the portfolio’s value each year, typically adjusted for inflation. This combines elements of both fixed and variable income strategies, providing a balance between predictability and flexibility. For instance, a retiree might withdraw 3% of their portfolio’s value annually, adjusted upwards each year to account for inflation. This offers a relatively stable income stream while aiming to preserve capital for the long term.

Tax Implications of Retirement Withdrawals

Understanding the tax implications of your retirement withdrawals is critical for effective financial planning. Different retirement accounts have different tax treatments.

- Traditional IRAs and 401(k)s: Withdrawals from these accounts are generally taxed as ordinary income. This means they are taxed at your regular income tax bracket.

- Roth IRAs: Withdrawals from Roth IRAs are generally tax-free, provided the account has been open for at least five years and the withdrawals are considered qualified (meaning they are after age 59 1/2).

- Tax-Deferred Annuities: Withdrawals from annuities are taxed as ordinary income, but the tax liability may vary depending on the type of annuity and the timing of withdrawals.

Careful tax planning can significantly impact your retirement income. Consult with a financial advisor to understand the tax implications of your specific situation and develop a tax-efficient withdrawal strategy.

Securing a comfortable retirement requires careful planning and proactive investment strategies. By understanding your goals, assessing your risk tolerance, and diversifying your portfolio, you can build a solid foundation for financial security. Remember to regularly review and adjust your plan as needed, seeking professional advice when necessary. Your future self will thank you for the effort invested today.

FAQs

What is the difference between a 401(k) and a Roth IRA?

A 401(k) is a retirement savings plan sponsored by your employer, often with matching contributions. A Roth IRA is a personal retirement account where contributions are made after tax, but withdrawals in retirement are tax-free.

How much should I save for retirement?

The amount you need to save depends on your lifestyle goals, retirement age, and life expectancy. A common rule of thumb is to aim for saving at least 10-15% of your pre-tax income.

When should I start withdrawing from my retirement accounts?

You can typically begin withdrawing from traditional retirement accounts at age 59 1/2, though penalties may apply for early withdrawals. The age for penalty-free withdrawals from Roth IRAs depends on the contribution rules.

What is the role of a financial advisor?

A financial advisor provides personalized guidance on investment strategies, risk management, and retirement planning. They can help you create a tailored plan based on your individual circumstances and goals.