Navigating the world of investments can feel overwhelming, but what if your financial journey was tailored to your specific needs and goals? Personalized investment advice offers a unique approach, moving beyond generic strategies to create a bespoke plan designed for your individual circumstances. This involves a deep dive into your financial situation, risk tolerance, and aspirations to craft a portfolio optimized for your success.

This personalized approach leverages advanced data analysis, sophisticated algorithms, and a thorough understanding of your unique financial landscape. From understanding your risk profile to selecting appropriate asset classes and implementing robust strategies for growth and preservation, the aim is to achieve your financial objectives while mitigating potential risks. This exploration will delve into the regulatory frameworks, technological advancements, and ethical considerations that underpin this increasingly crucial financial service.

Defining Personalized Investment Advice

Personalized investment advice tailors investment strategies to an individual’s unique circumstances, goals, and risk tolerance. Unlike generic advice, it considers a holistic view of the investor’s financial life, leading to more effective and suitable investment plans.Personalized investment advice comprises several core components. These include a thorough understanding of the client’s financial situation (assets, liabilities, income, expenses), their investment goals (retirement, education, etc.), their risk tolerance and time horizon, and their overall financial objectives.

This information forms the basis for creating a customized investment portfolio designed to meet their specific needs.

Core Components of Personalized Investment Advice

A comprehensive understanding of the client’s financial situation is paramount. This involves a detailed assessment of their assets (e.g., savings, real estate, investments), liabilities (e.g., loans, mortgages), income, and expenses. This data provides a clear picture of their net worth and cash flow, which are crucial for developing a suitable investment strategy. Additionally, defining the client’s investment goals – whether short-term or long-term – is essential.

Understanding their risk tolerance, which represents their comfort level with potential investment losses, is another key element. Finally, aligning the investment strategy with their overall financial objectives ensures the plan remains consistent with their broader life goals.

Personalized vs. Generic Investment Advice

The key difference lies in the level of customization. Generic investment advice provides generalized recommendations applicable to a broad range of investors, often based on market trends or broad asset allocation strategies. For example, a generic recommendation might suggest a 60/40 stock-bond portfolio for all investors. Personalized advice, however, tailors the asset allocation, investment choices, and risk management strategies to the individual’s specific profile.

A high-net-worth individual with a long time horizon and high risk tolerance might receive a significantly different portfolio recommendation compared to a retiree with a low risk tolerance and shorter time horizon, even if both seek similar financial outcomes. This individualized approach maximizes the potential for achieving the client’s specific goals while minimizing unnecessary risk.

Approaches to Delivering Personalized Investment Advice

Several approaches exist for delivering personalized investment advice. Traditional methods involve face-to-face meetings with financial advisors who conduct thorough assessments and develop customized plans. Robo-advisors, on the other hand, leverage technology to provide automated, algorithm-driven advice based on client-provided information. Hybrid models combine the personalized touch of human advisors with the efficiency of technology, often utilizing digital tools for portfolio management and communication.

Each approach offers varying degrees of personalization and cost-effectiveness. For example, traditional financial advisors often provide more comprehensive and nuanced advice but come with higher fees, while robo-advisors offer more affordable options but may lack the personalized attention of human advisors.

Technology’s Enhancement of Personalized Investment Advice

Technology significantly enhances personalized investment advice in several ways. Sophisticated algorithms can analyze vast datasets to identify optimal investment strategies based on individual risk profiles and goals. Portfolio management software facilitates efficient rebalancing and monitoring of investments. Digital platforms enable seamless communication and information sharing between advisors and clients, fostering better collaboration and transparency. For example, robo-advisors utilize algorithms to dynamically adjust portfolios based on market conditions and client goals, providing continuous optimization.

Furthermore, online portals allow clients to access their account information, track their investments, and communicate with their advisors at any time. This increased accessibility and transparency empowers clients to actively participate in the management of their investments.

Investment Strategies and Portfolio Construction

Personalized investment advice hinges on crafting a portfolio tailored to a client’s specific financial goals, risk tolerance, and time horizon. This involves selecting appropriate investment strategies and constructing a portfolio that balances risk and return effectively. Understanding the interplay between these elements is crucial for achieving long-term financial success.

Investment Strategies for Different Client Profiles

Different investment strategies cater to diverse client needs. Conservative investors, typically those nearing retirement or with low risk tolerance, may favor strategies focused on capital preservation and income generation. These strategies often involve a higher allocation to bonds, fixed-income securities, and low-volatility stocks. Conversely, aggressive investors, often younger individuals with a longer time horizon and higher risk tolerance, may adopt strategies emphasizing growth and capital appreciation, with a larger allocation to equities, including growth stocks and emerging markets.

Moderate investors occupy a middle ground, balancing risk and return through a diversified portfolio that incorporates both stocks and bonds. The specific asset allocation within each strategy is adjusted based on individual circumstances and market conditions.

Portfolio Construction Methodologies

Several methodologies guide portfolio construction. Modern Portfolio Theory (MPT) emphasizes diversification to minimize risk while maximizing returns. It involves calculating the efficient frontier, which represents the optimal combination of risk and return for a given portfolio. Value investing focuses on identifying undervalued securities based on fundamental analysis, aiming for long-term capital appreciation. Growth investing prioritizes companies expected to experience rapid growth, potentially at higher risk.

Factor-based investing considers specific factors like value, size, and momentum to identify stocks likely to outperform the market. The choice of methodology depends on the client’s investment goals and risk profile.

Adjusting Portfolio Allocation Based on Market Conditions

Market conditions significantly influence portfolio allocation. During periods of economic uncertainty or market downturns, a more conservative approach may be warranted, potentially involving a shift towards lower-risk assets like government bonds or cash. Conversely, during periods of economic expansion and market growth, investors may increase their allocation to higher-risk, higher-return assets like equities. This dynamic adjustment requires ongoing monitoring of market trends and economic indicators, alongside regular review of the client’s financial goals and risk tolerance.

For instance, during the 2008 financial crisis, many investors shifted their portfolios towards safer assets to mitigate losses.

Sample Portfolio for a Hypothetical Client

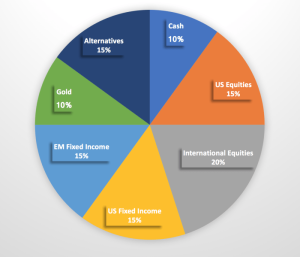

This example illustrates a sample portfolio for a 40-year-old client with a moderate risk tolerance and a long-term investment horizon (20 years). The goal is long-term capital growth with moderate income generation.

| Asset Class | Allocation Percentage | Rationale | Risk Level |

|---|---|---|---|

| US Equities | 40% | Provides core exposure to the US market, offering potential for long-term growth. | Moderate |

| International Equities | 20% | Diversifies geographically, reducing risk and potentially enhancing returns. | Moderate to High |

| Bonds (Investment Grade) | 30% | Provides stability and income, mitigating overall portfolio risk. | Low |

| Real Estate (REITs) | 10% | Offers diversification and potential for inflation hedging. | Moderate |

Investment Advice

Providing personalized investment advice extends far beyond simply constructing a portfolio. It’s a dynamic process requiring ongoing engagement and a commitment to ethical practice. Success hinges on consistent monitoring, transparent communication, and a deep understanding of the psychological factors influencing investor behavior.Ongoing Portfolio Monitoring and RebalancingRegular monitoring and rebalancing are crucial for maintaining a portfolio’s alignment with the client’s financial goals and risk tolerance.

Market fluctuations constantly shift asset allocations, potentially derailing a well-crafted strategy. Rebalancing involves adjusting the portfolio’s asset classes back to their target weights, selling some assets that have outperformed and buying others that have underperformed. This disciplined approach helps to capitalize on market inefficiencies and mitigate risk. For example, if a client’s portfolio has a target allocation of 60% stocks and 40% bonds, and the stock market experiences a significant rally, the portfolio might become 70% stocks and 30% bonds.

Rebalancing would involve selling some stocks and buying bonds to restore the original 60/40 allocation. This process helps to prevent excessive risk-taking during bull markets and limits losses during bear markets.

Effective Communication with Clients

Maintaining open and transparent communication is paramount. Regular updates, easily understandable reports, and readily available channels for questions are essential. Clients should understand their investment strategy, the rationale behind portfolio choices, and the potential risks and rewards. Explaining investment performance in context, avoiding overly technical jargon, and proactively addressing concerns foster trust and a strong advisor-client relationship.

For example, a quarterly report might include a summary of portfolio performance, a comparison to relevant benchmarks, and a discussion of any significant market events or adjustments made to the portfolio. Providing multiple communication channels, such as email, phone, and scheduled in-person meetings, ensures accessibility and caters to individual client preferences.

Ethical Considerations in Investment Advice

Ethical conduct is the cornerstone of trustworthy investment advice. Fiduciary duty, which prioritizes the client’s best interests above all else, is paramount. This includes transparency about fees, conflicts of interest, and any limitations of the advice provided. Adherence to regulatory standards and a commitment to ongoing professional development are crucial for maintaining ethical standards. For example, an advisor should disclose any commissions or incentives they receive from recommending specific investments.

Furthermore, they should avoid recommending investments that are not suitable for the client’s risk profile or financial goals, even if those investments might generate higher commissions for the advisor. Transparency and integrity build trust and long-term client relationships.

Behavioral Finance and Investment Decision-Making

Behavioral finance acknowledges the impact of psychological biases on investment decisions. Understanding these biases, such as overconfidence, loss aversion, and herd mentality, is critical for advisors. Advisors can help clients mitigate the negative effects of these biases through education, careful planning, and a long-term investment perspective. For instance, an advisor might help a client who is experiencing loss aversion by reminding them of their long-term financial goals and the importance of staying invested during market downturns.

They might also help clients avoid making impulsive decisions based on short-term market fluctuations by emphasizing the importance of a well-diversified portfolio and a long-term investment strategy. By recognizing and addressing these behavioral tendencies, advisors can guide clients toward more rational and effective investment choices.

Future Trends in Personalized Investment Advice

The landscape of personalized investment advice is poised for significant transformation in the coming years, driven by rapid technological advancements and evolving client expectations. This evolution will redefine the advisor-client relationship and reshape how investment strategies are developed and implemented.The convergence of several powerful forces will shape the future of this field. These include the increasing sophistication of artificial intelligence, the proliferation of data analytics capabilities, and the ongoing democratization of financial information.

Emerging Technologies Shaping Personalized Investment Advice

Artificial intelligence (AI), machine learning (ML), and natural language processing (NLP) are rapidly changing how personalized investment advice is generated and delivered. AI algorithms can analyze vast datasets of market data, economic indicators, and individual client profiles to create highly customized investment portfolios. ML models can learn from past performance and adapt investment strategies in real-time, responding to market fluctuations more effectively than traditional methods.

NLP allows for more natural and intuitive interactions between clients and digital advisory platforms, making the process more accessible and engaging. For example, robo-advisors are already utilizing AI to provide basic portfolio management based on risk tolerance and financial goals, and this technology will continue to become more sophisticated, offering more nuanced and tailored advice.

Fintech’s Impact on Personalized Investment Advice Delivery

Fintech companies are disrupting the traditional financial services industry by offering innovative and often more affordable solutions for personalized investment advice. These solutions range from robo-advisors that provide automated portfolio management to sophisticated platforms that combine AI-powered analytics with human advisor support. The accessibility and convenience offered by fintech platforms are attracting a broader range of investors, particularly younger generations who are comfortable interacting with technology.

The increased competition among fintech firms is also driving innovation and pushing down fees, making personalized investment advice more accessible to a wider population. Consider the rise of mobile-first investment platforms, which offer seamless account management and real-time portfolio updates, illustrating the transformative impact of fintech.

The Evolving Role of Financial Advisors in an Automated Landscape

While automation is increasing, the role of human financial advisors is not becoming obsolete; instead, it is evolving. Financial advisors will increasingly focus on higher-value activities such as complex financial planning, estate planning, and providing emotional support and guidance to clients. They will leverage technology to enhance their efficiency and effectiveness, allowing them to serve a larger client base while maintaining a high level of personalized service.

The advisor-client relationship will shift from a transactional model to a more consultative partnership, with advisors acting as trusted guides navigating complex financial decisions. Examples of this evolution include advisors using AI-powered tools to analyze client data and identify potential opportunities, freeing up their time for more strategic conversations.

Visual Representation of the Evolution of Personalized Investment Advice

Imagine a graph charting the evolution of personalized investment advice over the next decade. The X-axis represents time, spanning from the present to ten years in the future. The Y-axis represents the level of personalization and automation. The graph begins with a relatively flat line, representing the current state where personalization is limited and automation is nascent.

Over the next decade, the line sharply increases, showing a rapid rise in both personalization and automation. However, the line doesn’t become perfectly vertical; it curves upward, illustrating that while automation increases significantly, the human element, represented by the financial advisor’s expertise and personalized touch, remains crucial and interwoven with technology. The final point on the graph is significantly higher than the starting point, showcasing a future where highly personalized and automated investment advice is the norm, yet still delivered with the essential human element.

Ultimately, personalized investment advice empowers individuals to take control of their financial future. By combining sophisticated technology with human expertise, this approach allows for a more efficient and effective path towards achieving financial goals. While technology plays a significant role in automating processes and analyzing data, the human element remains crucial, providing guidance, interpreting complex information, and ensuring ethical considerations are always at the forefront.

The future of personalized investment advice promises even greater efficiency and personalization, further enhancing the investor experience and fostering better financial outcomes.

Query Resolution

What is the cost of personalized investment advice?

Costs vary greatly depending on the advisor, services offered, and asset size under management. Fees can be based on assets under management (AUM), hourly rates, or a combination of both.

How often should I review my personalized investment plan?

Regular reviews, at least annually, are recommended to assess performance, adjust for life changes, and rebalance your portfolio as needed. More frequent reviews may be appropriate depending on market volatility or significant life events.

What if my financial situation changes significantly?

It’s crucial to inform your advisor immediately of any major changes, such as job loss, inheritance, or significant debt. Your investment strategy may need adjustment to reflect your new circumstances.

How can I find a reputable personalized investment advisor?

Thorough research is key. Check credentials, certifications, experience, and client reviews. Consider seeking referrals from trusted sources and verifying their regulatory compliance.