Navigating the complex world of high-net-worth individual (HNWI) investments requires a nuanced understanding of diverse asset classes, tax implications, and risk management strategies. This guide delves into the unique financial needs of HNWIs, exploring sophisticated investment vehicles and the crucial role of experienced financial advisors in achieving long-term financial goals. We’ll examine alternative investment strategies, portfolio construction techniques, and the importance of proactive tax planning to help preserve and grow wealth.

From understanding the specific challenges and opportunities facing HNWIs to developing robust, diversified portfolios, we aim to provide a comprehensive overview of best practices in wealth management. This includes a discussion of ethical considerations for financial advisors, risk tolerance assessment, and the importance of due diligence in investment decision-making. Ultimately, our goal is to equip readers with the knowledge necessary to make informed choices and navigate the complexities of HNWI wealth management effectively.

Risk Management and Portfolio Construction for HNWIs

High-net-worth individuals (HNWIs) face unique challenges in managing their wealth, requiring sophisticated strategies that balance growth potential with the preservation of capital. Effective risk management is paramount, going beyond simply minimizing losses to actively shaping the portfolio’s resilience against various market conditions and personal circumstances. This involves a comprehensive understanding of risk tolerance, strategic asset allocation, and the utilization of diverse risk mitigation tools.

Risk Tolerance Assessment for HNWIs

Determining an HNWI’s risk tolerance is a crucial first step. It’s not simply a matter of their net worth; it involves a deep dive into their financial goals, time horizon, lifestyle needs, and emotional response to market fluctuations. A comprehensive assessment should consider both quantitative factors (e.g., investable assets, income sources, debt levels) and qualitative factors (e.g., risk aversion, comfort with potential losses, legacy planning objectives).

For example, an HNWI nearing retirement with significant wealth might have a lower risk tolerance than a younger individual with a longer time horizon and greater earning potential. Professional financial advisors often use questionnaires and interviews to gauge risk tolerance, tailoring the assessment to the individual’s unique circumstances. This process ensures that the investment strategy aligns with their comfort level and overall financial objectives.

Portfolio Construction Strategies for Mitigating Risk

Diversification is a cornerstone of risk mitigation for HNWIs. This goes beyond simply holding different asset classes (stocks, bonds, real estate, etc.). It requires a nuanced approach, considering geographic diversification (investing across different countries), sector diversification (avoiding overexposure to specific industries), and even diversification within asset classes (e.g., investing in different types of bonds or real estate properties). For example, a portfolio might include a mix of domestic and international equities, government and corporate bonds, private equity, hedge funds, and alternative investments like commodities or infrastructure.

Strategic asset allocation, based on the HNWI’s risk tolerance and financial goals, is crucial for determining the optimal proportion of each asset class. This allocation is regularly reviewed and adjusted to reflect changes in market conditions and the HNWI’s circumstances.

The Role of Insurance and Other Risk Management Tools

Insurance plays a vital role in protecting an HNWI’s wealth from unforeseen events. This includes comprehensive liability insurance, property insurance, and potentially key-person insurance for businesses. Beyond insurance, other risk management tools include hedging strategies (such as options or futures contracts) to protect against specific market risks, and sophisticated tax planning to minimize tax liabilities. For instance, a high-net-worth entrepreneur might utilize key-person insurance to protect the business’s value in the event of their death or disability, ensuring the continuity of the enterprise and safeguarding the family’s wealth.

Similarly, employing tax-efficient investment structures can significantly reduce the overall tax burden, preserving more of the accumulated wealth.

Building a Diversified and Risk-Managed Portfolio: A Step-by-Step Process

- Comprehensive Financial Planning: Begin with a detailed assessment of the HNWI’s financial situation, goals, and risk tolerance. This includes evaluating their assets, liabilities, income streams, and future financial needs (retirement, education, legacy planning).

- Asset Allocation Strategy: Based on the financial plan, develop a strategic asset allocation that aligns with the HNWI’s risk profile and objectives. This will define the target percentages for each asset class.

- Investment Selection: Choose specific investments within each asset class, ensuring diversification across sectors, geographies, and investment vehicles.

- Risk Mitigation Strategies: Implement appropriate risk mitigation strategies, including insurance, hedging, and tax planning, to protect against potential losses.

- Portfolio Monitoring and Rebalancing: Regularly monitor the portfolio’s performance and rebalance it as needed to maintain the target asset allocation. This involves selling some assets that have outperformed and buying others that have underperformed.

- Periodic Review and Adjustment: Conduct periodic reviews of the financial plan and investment strategy, adjusting it as the HNWI’s circumstances or market conditions change.

The Role of Financial Advisors in Serving HNWIs

High-net-worth individuals (HNWIs) require specialized financial guidance due to the complexity of their financial situations. Their needs extend beyond basic investment management and encompass sophisticated tax planning, estate preservation, and philanthropic endeavors. Selecting the right financial advisor is crucial for achieving their financial goals and safeguarding their wealth.Financial advisors working with HNWIs possess a distinct set of expertise and qualifications.

They typically hold advanced professional designations, such as a Certified Financial Planner (CFP), Chartered Financial Analyst (CFA), or similar credentials, demonstrating a commitment to ongoing professional development and a high level of financial acumen. Beyond certifications, extensive experience managing complex portfolios and a deep understanding of various asset classes, including alternative investments, are essential. Furthermore, a strong network of legal, tax, and other professional advisors is crucial for holistic wealth management.

Expertise and Qualifications of Financial Advisors for HNWIs

Advisors serving HNWIs must possess a broad range of skills and knowledge. They need expertise in investment management across various asset classes, including stocks, bonds, real estate, private equity, and hedge funds. Furthermore, a thorough understanding of tax implications for high-income individuals and sophisticated estate planning strategies is vital. Strong communication and interpersonal skills are essential for building trust and rapport with clients, and the ability to navigate complex financial situations with clarity and precision is paramount.

Finally, advisors must stay abreast of evolving market trends and regulatory changes to provide effective and compliant advice.

Fiduciary Duty and Ethical Considerations for Advisors Serving HNWIs

A cornerstone of the advisor-client relationship is the fiduciary duty. This legal and ethical obligation requires advisors to act in the best interests of their clients, prioritizing their needs above their own. This includes full transparency regarding fees, conflicts of interest, and investment strategies. Ethical considerations extend to maintaining client confidentiality, avoiding conflicts of interest, and adhering to strict regulatory standards.

For HNWIs, where the financial stakes are exceptionally high, the fiduciary duty is paramount, demanding unwavering commitment to ethical conduct and client well-being. Breaches of fiduciary duty can have serious legal and reputational consequences.

Fee Structures Used by Financial Advisors Serving HNWIs

Financial advisors serving HNWIs employ various fee structures, each with its own advantages and disadvantages. A common approach is the fee-based advisory model, where clients pay an annual fee based on a percentage of assets under management (AUM). This structure provides ongoing advisory services and is often preferred for its transparency. Alternatively, some advisors utilize a commission-based model, earning fees from the sale of financial products.

While simpler in structure, this model can potentially create conflicts of interest if the advisor’s incentives are misaligned with the client’s best interests. Finally, some advisors offer a hybrid model, combining aspects of both fee-based and commission-based structures. The selection of the most appropriate fee structure depends on individual client needs and preferences, with a focus on transparency and alignment of interests.

Best Practices for Selecting a Suitable Financial Advisor for HNWI Needs

Choosing a financial advisor is a critical decision for HNWIs. A thorough due diligence process is essential. This includes carefully vetting the advisor’s credentials, experience, and reputation. Checking references, reviewing client testimonials, and understanding the advisor’s investment philosophy are all important steps. It’s also crucial to clarify the fee structure, understand any potential conflicts of interest, and ensure the advisor’s expertise aligns with the client’s specific financial goals and risk tolerance.

Regular communication and performance reviews are essential for maintaining a strong and productive advisor-client relationship. Finally, seeking a second opinion can be beneficial to ensure a well-rounded perspective on investment strategies and financial planning.

Investment Advice

Sound investment advice for high-net-worth individuals (HNWIs) goes beyond simply maximizing returns. It’s a holistic approach that considers an individual’s unique financial situation, risk tolerance, and long-term goals. This involves a deep understanding of various asset classes, market dynamics, and a commitment to prudent risk management.Core Principles of Sound Investment Advice

Due Diligence and Thorough Research

Effective investment decisions hinge on meticulous due diligence and comprehensive research. This involves a thorough examination of potential investments, including financial statements, market analysis, and competitive landscapes. For example, before investing in a private equity fund, a thorough review of the fund manager’s track record, investment strategy, and portfolio companies is crucial. Similarly, evaluating a real estate investment requires detailed property assessments, market research, and analysis of potential rental income and appreciation.

Neglecting this step can lead to significant financial losses.

Time Horizon and Investment Strategy

The investment time horizon, or the length of time an investor plans to hold an investment, significantly impacts investment strategy. Short-term investors, with a time horizon of less than one year, might prioritize liquidity and capital preservation, focusing on low-risk investments like money market funds or government bonds. Conversely, long-term investors, with a horizon of 10 years or more, can afford to take on more risk in pursuit of higher returns, potentially including investments in equities or alternative assets.

Consider the example of a young professional with a long time horizon who can invest in high-growth stocks, accepting the higher risk for potentially greater long-term gains. In contrast, a retiree nearing the end of their working life might prioritize income generation and capital preservation, favouring lower-risk investments.

Assessing Investment Suitability

Determining the suitability of an investment depends on a multitude of factors unique to each individual. This includes their risk tolerance, financial goals, investment experience, and existing portfolio diversification. A conservative investor with a low risk tolerance might find a diversified portfolio of bonds and blue-chip stocks more suitable than highly speculative investments. Conversely, an aggressive investor with a high risk tolerance and a longer time horizon might find alternative investments like venture capital or private equity more appealing, despite their inherent higher risk.

A financial advisor plays a critical role in guiding HNWIs through this assessment, ensuring that investments align with their overall financial plan and risk profile. For example, an advisor would help a client nearing retirement understand the trade-off between higher returns and potential losses, guiding them toward a strategy that balances their need for income with their risk aversion.

Illustrative Case Study

This case study presents a hypothetical investment portfolio for a high-net-worth individual (HNWI) with a long-term investment horizon and a moderate risk tolerance. The portfolio aims for diversification across asset classes to mitigate risk and generate consistent returns. It’s important to note that this is a sample portfolio and individual circumstances should always dictate specific investment strategies. Professional financial advice should be sought before making any investment decisions.

The following portfolio allocation considers the HNWI’s risk profile and financial goals, balancing growth potential with capital preservation. It emphasizes a diversified approach across various asset classes, seeking to minimize overall portfolio volatility while aiming for long-term capital appreciation.

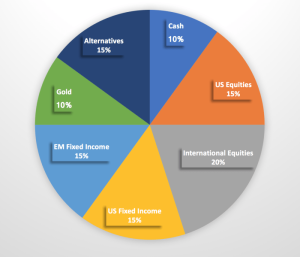

Sample HNWI Investment Portfolio Allocation

The proposed portfolio allocates assets across several major asset classes to achieve diversification and balance risk and reward. The percentages represent the target allocation, and adjustments may be necessary based on market conditions and individual circumstances. Regular rebalancing is crucial to maintain the desired asset allocation.

- Equities (40%): This portion is further diversified across both domestic and international markets, including a mix of large-cap, mid-cap, and small-cap stocks. This allocation provides exposure to growth opportunities and long-term capital appreciation. The inclusion of international equities helps to reduce overall portfolio risk by diversifying geographically and reducing exposure to any single national market’s economic fluctuations. A portion of this allocation might also be directed towards actively managed funds and the remainder to passively managed index funds, aiming to balance active management’s potential for outperformance with the cost-effectiveness and diversification benefits of index funds.

- Fixed Income (30%): This component includes a mix of government bonds, corporate bonds, and high-yield bonds, offering a balance between stability and yield. Government bonds provide stability and safety, acting as a ballast during periods of market uncertainty. Corporate bonds offer potentially higher yields but come with higher credit risk. High-yield bonds offer even higher yields but carry significantly more risk.

The precise allocation within fixed income will depend on the HNWI’s risk tolerance and overall financial goals. A laddered approach to bond maturity dates can help to mitigate interest rate risk.

- Alternative Investments (15%): This portion might include investments in real estate, private equity, hedge funds, or commodities. Alternative investments offer the potential for diversification and higher returns but usually involve higher levels of illiquidity and risk. Real estate investments can provide a hedge against inflation and a stream of rental income, while private equity offers access to growth opportunities in companies not publicly traded.

Hedge funds employ complex strategies to generate returns, often seeking to profit from market inefficiencies. Commodities, such as gold or oil, can act as a hedge against inflation and geopolitical uncertainty.

- Cash and Cash Equivalents (10%): This allocation serves as a buffer for unexpected expenses and investment opportunities. This liquid component allows for flexibility and minimizes the need to sell other assets at unfavorable times to meet immediate needs. It could include money market funds, certificates of deposit, and high-yield savings accounts.

- Precious Metals (5%): A small allocation to precious metals like gold can act as a hedge against inflation and geopolitical uncertainty. Gold’s price often moves inversely to the stock market, providing a degree of diversification and risk reduction. This allocation should be viewed as a portfolio diversifier and not a primary source of return.

Potential Risks and Rewards

This portfolio, while diversified, is not without risk. The inherent volatility of the market means that losses are possible, particularly in the short term. However, the diversification strategy aims to mitigate these risks and improve the chances of long-term success.

Potential rewards include long-term capital appreciation across all asset classes, consistent income generation from fixed income and real estate, and diversification benefits that help to cushion against market downturns. The alternative investments component offers the potential for higher returns, but also carries a greater degree of risk.

Impact of Different Market Scenarios

Bull Market Scenario: In a bull market characterized by rising stock prices, the equity portion of the portfolio would likely experience significant growth. Fixed income would likely see moderate gains, while alternative investments could see varying levels of appreciation. The overall portfolio performance would be positive, but the rate of return would be influenced by the specific performance of each asset class.

Bear Market Scenario: During a bear market, characterized by falling stock prices, the equity portion would likely experience losses. Fixed income, particularly government bonds, would likely provide some stability, acting as a buffer against the overall portfolio decline. Alternative investments could experience losses as well, but their performance would likely vary significantly based on the specific asset class. The overall portfolio would likely experience a decline, but the diversification would limit the extent of the losses compared to a portfolio heavily weighted in equities.

Stagnant Market Scenario: In a stagnant market, characterized by low or no growth, returns across all asset classes would likely be muted. The portfolio would experience minimal growth, but losses would also be limited. The cash and cash equivalents component would retain its value, providing stability during a period of market inactivity.

Successfully managing wealth for high-net-worth individuals demands a proactive and holistic approach. By carefully considering individual financial goals, employing sophisticated investment strategies, and leveraging the expertise of qualified financial advisors, HNWIs can effectively mitigate risk, optimize tax efficiency, and build a secure financial future. Understanding the nuances of alternative investments, the importance of diversification, and the ethical responsibilities of financial professionals are key to long-term success in this arena.

This guide serves as a foundational resource for navigating the intricacies of HNWI wealth management, empowering individuals to make informed decisions and achieve their financial aspirations.

Questions Often Asked

What is the difference between a financial advisor and a wealth manager?

While the terms are often used interchangeably, wealth managers typically handle a broader range of financial services, including estate planning and tax optimization, for high-net-worth individuals, whereas financial advisors may focus more narrowly on investment strategies.

How often should a HNWI review their investment portfolio?

Regular portfolio reviews are crucial, ideally at least annually, or more frequently depending on market volatility and personal circumstances. Significant life events or changes in financial goals necessitate more immediate review.

What are some common red flags to watch out for when choosing a financial advisor?

Red flags include high-pressure sales tactics, a lack of transparency regarding fees, unrealistic promises of high returns, and a failure to provide comprehensive financial planning.

What role does philanthropy play in HNWI investment strategies?

Philanthropic giving is often integrated into HNWI financial plans, sometimes through charitable trusts or foundations, which can offer tax advantages and provide a structured approach to charitable contributions.