Navigating the stock market can feel like charting uncharted waters, but with the right knowledge and strategy, achieving financial success is within reach. This guide provides a comprehensive overview of investment basics, risk management, and diverse strategies to help you build a robust portfolio tailored to your financial goals and risk tolerance. We’ll explore various investment approaches, from value investing to index funds, equipping you with the tools to make informed decisions and navigate market trends effectively.

Understanding the ethical considerations and seeking professional advice when needed are also crucial aspects we’ll cover.

From assessing your personal risk profile to diversifying your assets across different classes, we’ll walk you through a step-by-step process to help you build confidence and achieve your investment objectives. We’ll demystify complex financial concepts, making them accessible and understandable for both novice and experienced investors alike. Ultimately, our aim is to empower you to take control of your financial future.

Building a Diversified Portfolio

Diversification is a cornerstone of successful long-term investing. It’s the strategy of spreading your investments across various asset classes to reduce risk and potentially enhance returns. By not putting all your eggs in one basket, you mitigate the impact of any single investment performing poorly. This approach is crucial for achieving your financial goals while managing the inherent volatility of the market.Diversification is achieved through asset allocation, the process of determining how much of your portfolio should be invested in each asset class.

Asset allocation is paramount in managing risk because different asset classes react differently to market conditions. For example, stocks generally perform better during economic growth, while bonds can provide stability during downturns. A well-structured asset allocation strategy considers your risk tolerance, investment timeframe, and financial goals.

Asset Allocation and Risk Management

Effective asset allocation is the key to managing risk within your investment portfolio. A portfolio heavily weighted towards stocks, for example, will experience higher volatility but potentially higher returns over the long term. Conversely, a portfolio dominated by bonds will be less volatile but may offer lower returns. The optimal balance depends entirely on the investor’s individual circumstances.

Understanding your risk tolerance – your comfort level with potential losses – is crucial in determining your asset allocation. A younger investor with a longer time horizon might tolerate more risk and allocate a larger portion of their portfolio to stocks, while an older investor nearing retirement might prefer a more conservative approach with a greater emphasis on bonds and less risky assets.

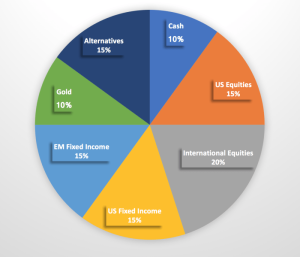

Sample Portfolio Allocation Strategy

This example illustrates a potential portfolio allocation for a hypothetical investor with a moderate risk tolerance and a long-term investment horizon (15+ years). This is for illustrative purposes only and should not be considered financial advice. Individual circumstances vary significantly.

- Stocks (Equities): 60% This includes a mix of large-cap, mid-cap, and small-cap stocks across different sectors (technology, healthcare, consumer goods, etc.) to further diversify within the equity asset class. This allocation aims to capture the potential for higher long-term growth.

- Bonds (Fixed Income): 30% This portion provides stability and reduces overall portfolio volatility. The bonds could be a mix of government bonds, corporate bonds, and potentially some high-yield bonds for slightly higher returns but increased risk.

- Real Estate (Alternative Investments): 10% This could be achieved through direct property investment or real estate investment trusts (REITs). Real estate can provide diversification and potentially inflation-hedging properties.

Examples of Asset Classes, Returns, and Risks

Different asset classes offer varying potential returns and levels of risk. Past performance is not indicative of future results, and all investments carry risk.

| Asset Class | Potential Return | Risk |

|---|---|---|

| Stocks (Equities) | High (potentially 7-10% annually, historically) | High (potential for significant losses) |

| Bonds (Fixed Income) | Moderate (potentially 3-5% annually, historically) | Moderate (lower risk than stocks but still subject to interest rate fluctuations) |

| Real Estate | Moderate to High (depending on market conditions and property type) | Moderate to High (subject to market fluctuations, property taxes, and maintenance costs) |

| Commodities (Gold, Oil, etc.) | Variable (can be highly volatile) | High (prices can fluctuate significantly based on supply and demand) |

| Cash | Low (typically less than inflation) | Low (very safe but returns may not keep pace with inflation) |

Investing in the stock market presents both opportunities and challenges. By understanding fundamental concepts, developing a well-defined investment strategy, and consistently managing risk, you can significantly improve your chances of achieving long-term financial growth. Remember that seeking professional advice when needed and staying informed about market trends are key components of successful investing. This guide provides a solid foundation; however, consistent learning and adaptation are crucial in this ever-evolving landscape.

Begin building your financial future today with informed, strategic investments.

FAQ Section

What is the difference between a stock and a bond?

Stocks represent ownership in a company, offering potential for higher returns but also greater risk. Bonds are loans to a company or government, generally offering lower returns but less risk.

How often should I review my investment portfolio?

Ideally, you should review your portfolio at least annually, or more frequently if market conditions significantly change or your personal circumstances alter.

What is dollar-cost averaging?

Dollar-cost averaging is an investment strategy where you invest a fixed amount of money at regular intervals, regardless of market fluctuations, reducing the impact of volatility.

Where can I find reliable financial news and information?

Reputable sources include the Wall Street Journal, Bloomberg, and financial news websites from established media outlets. Always critically evaluate information from less-known sources.

What is a 401(k)?

A 401(k) is a retirement savings plan sponsored by employers, allowing pre-tax contributions that grow tax-deferred until retirement.